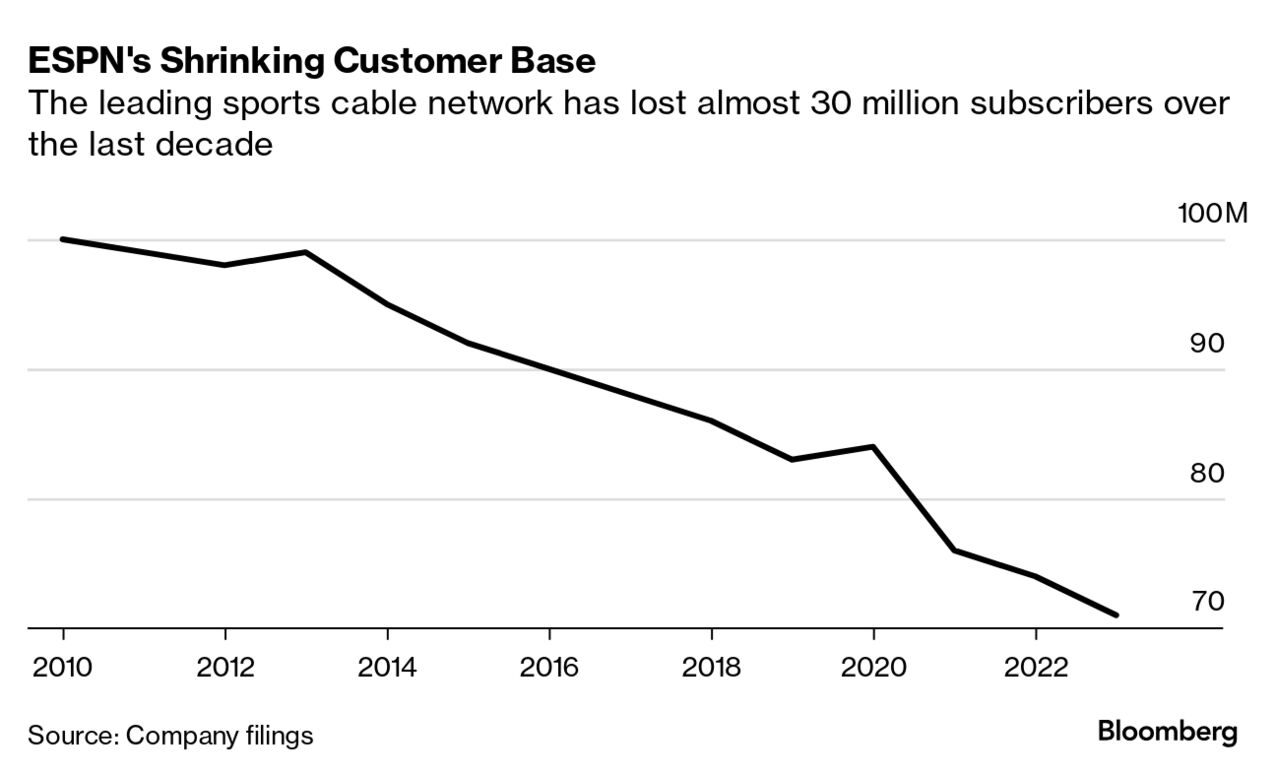

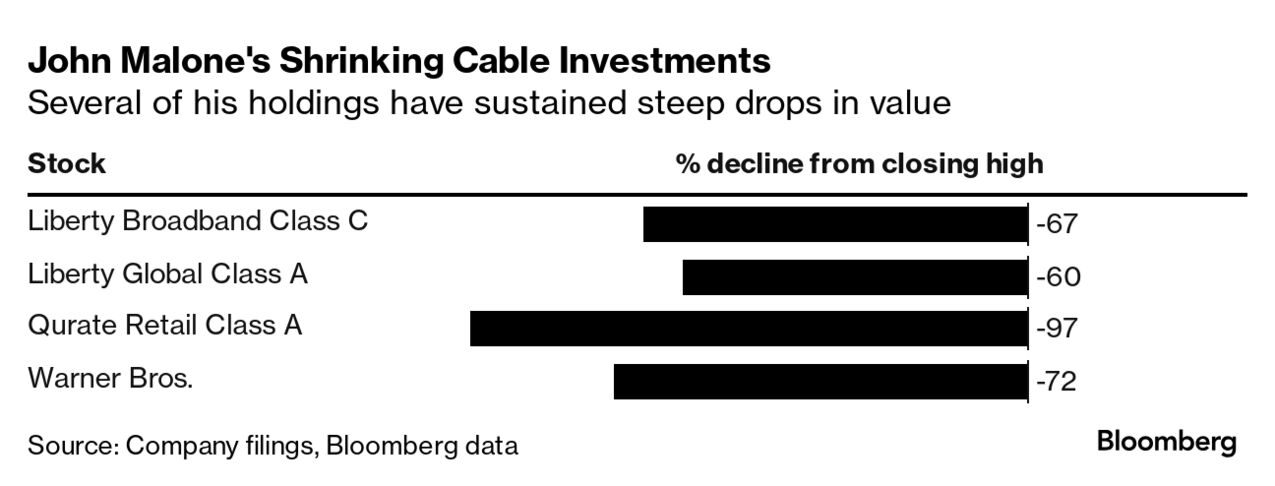

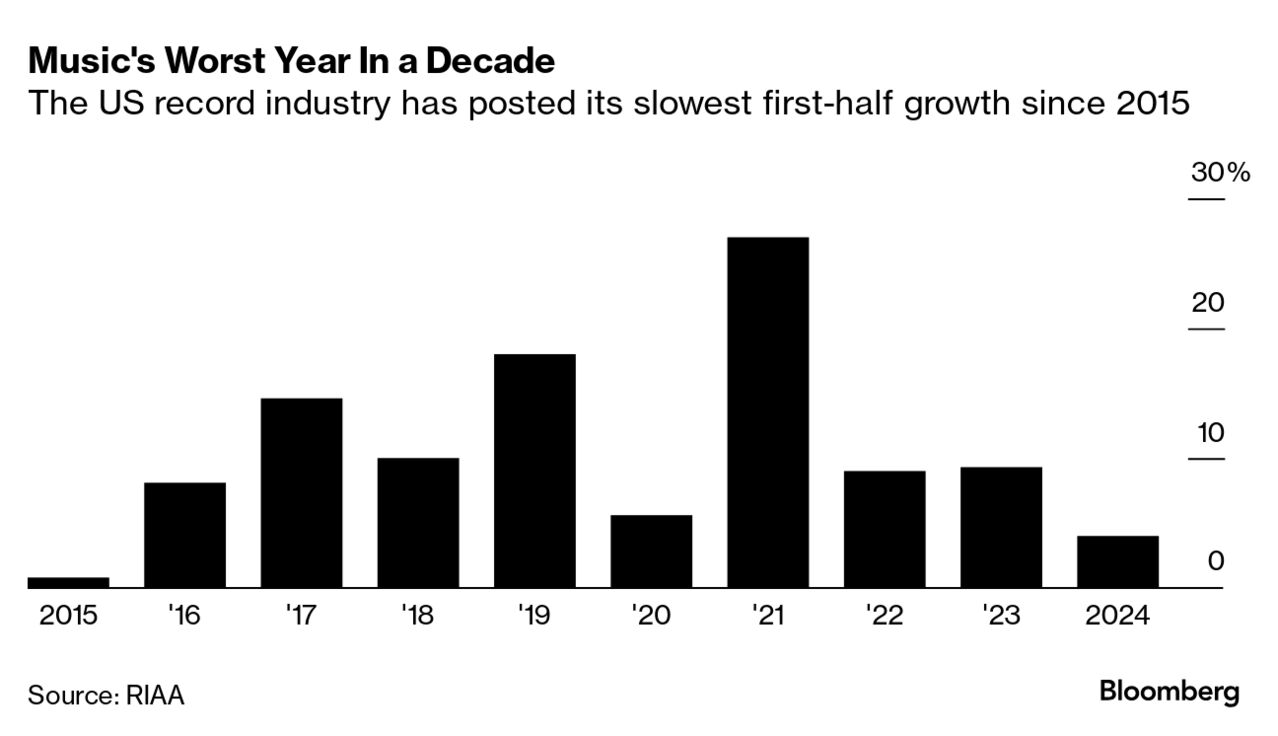

| The month of September means one thing to millions of Americans: football. The college season is underway, while the NFL starts this week. For the second year in a row, ESPN is locked in a contract dispute with one of its biggest business partners on the eve of the pro season. The sports media giant and satellite provider DirecTV have yet to comes to terms on a new distribution agreement, which means millions of customers have lost access to ESPN. Last year, the network went dark for customers of Charter Communications, the largest cable operator in the US. ESPN has long timed its contracts with pay-TV operators to expire around the start of football season, ensuring it has maximum leverage when negotiating new deals. But those negotiations have grown acrimonious in recent years as both pay-TV providers and networks struggle with the accelerating decline of their business. DirecTV wants to offer small bundles of Disney channels in genres like kids programming, news, movies and sports that will reduce costs for customers. Disney’s distribution chief, Justin Connolly, said he offered DirecTV a smaller sports package, as well as changes to other terms. No pay-TV operator wants to be without football, one of the few types of programming powerful enough to make someone change their service provider. Nor can ESPN withstand the loss of viewers or damage to its brand from depriving customers of their favorite sport. But the frequency of these disputes underscores the urgent challenge for ESPN, the world’s largest sports media company, as well as its owner, Walt Disney. ESPN charges cable operators more than any other network, which was great when cable was booming. Now it means every cord cutter costs ESPN more money than anyone else. Disney needs to make as much money as it can from the shrinking cable and satellite-TV market while expanding its other businesses. Last week, ESPN bused a few dozen reporters to its headquarters in Bristol, Connecticut, to make the case for the sports network’s future. ESPN Chairman Jimmy Pitaro kicked things off by sitting down for a conversation with his spokesperson, Josh Krulewitz, in which he stressed the importance of three initiatives: streaming, fantasy sports and gambling. ESPN’s streaming solutionsThe decline of pay-TV is not a new problem for ESPN. The network, which was early to embrace the internet with its website and social-media channels, has been trying to respond to cord cutting for years. It introduced the standalone streaming service ESPN+ in 2018. But it has yet to make its most popular sports, like football, available to customers who don’t pay for cable. That will happen in 2025. (It would sure be nice if ESPN could offer DirecTV customers that app right now.) Nicknamed “Flagship,” the service will integrate ESPN’s fantasy and betting platforms, and is on schedule to launch around this time next year. The biggest question surrounding “Flagship” will be the price. ESPN charges cable operators an average of less than $10 a month. This new service will need to cost a lot more because the customer base for ESPN is smaller than that for all of cable. But charge too much, and you alienate millions of people. Nobody at ESPN — not even Pitaro — can predict just how big their new streaming service will be. But he knows ESPN can’t replicate its cable network business, which peaked at 100 million customers, with just a standalone ESPN streaming service. That’s why he is pursuing several different streaming plans to offset the decline in the linear business. Disney is integrating ESPN more closely into the Disney+ streaming service and has partnered with Warner Bros. and Fox on Venu, which offers a bundle of sports-focused TV networks for $43 a month. The target audience for this service is small; it offers some events for about half the price of cable. Its owners have forecast 5 million customers in the first five years. That is, if it ever launches. On Aug. 16, a judge halted its debut. Pitaro disagrees with the judge’s decision that the platform is monopolistic. “We believe that Venu is a pro-competitive service,” he said. “It is pro-consumer, pro-sports fan, and we believe it’s giving the sports fan another option.” Other betsWhile most of the media day was carefully managed, Pat McAfee, who signed a multiyear agreement with the network last year, clashed with reporters over their coverage of him and accused one media outlet of stealing his content and posting it online as its own. “You made a lot of my life hell for a bit with the things you reported, how you reported it,” he told one reporter. The former Indianapolis Colts punter, who first began airing his eponymous show on YouTube, has drawn criticism over his comments about basketball star Caitlin Clark and an interview with Aaron Rodgers in which the New York Jets quarterback inaccurately implied that late night host Jimmy Kimmel had connections to sex offender Jeffrey Epstein. “It creates friction and problems from time to time when he says something or does something — that has to be managed, but the pros outweigh the cons,” Burke Magnus, ESPN’s president of content, said of McAfee during lunch with reporters. Pitaro also unveiled a new “Where to Watch” feature on the ESPN app and website to help fans find where a particular game is airing, even if it’s not on a company channel. The feature, along with ESPN’s licensing deal with casino operator Penn Entertainment, are among the company’s latest innovations. Players with Penn/ESPN Bet will be linked to their general ESPN account, enabling them to get betting information based on their sports-watching. ESPN is also rolling out custom betting offers based on users’ fantasy teams. ESPN’s business challenges have yet to slow its spending on major rights. It has the largest collection of events in the US and will remain a home of the NFL and NBA into the next decade. While observers keep waiting for the network to forgo some rights, it has renewed all of its biggest deals. For all the noise around talent like McAfee, fantasy and gambling, those rights are the best reason to believe in ESPN’s future. In the end, it came down to who had the most money. Filmmaker David Ellison, whose father, Oracle Corp. co-founder Larry, is worth $156 billion, is the winner. Absent any legal or regulatory hurdles, he’ll take over the parent of CBS, MTV and Paramount Pictures in the first half of next year, after agreeing to spend more than $8 billion buying Paramount shares and helping the company reduce its debt. Edgar Bronfman Jr., a longtime media investor and heir to the Seagram Co. liquor fortune, got a late start and came up short, with a tentative offer of $6 billion. Bain Capital, which invested with him the past, dropped out. Some 50 potential investor names were submitted by Bronfman so they could get a look at the company’s financials. But several, including Roku and Len Blavatnik’s Access Industries, chose not to join his effort. Bronfman was putting up about $100 million himself, according to one person with knowledge of the matter. BC Partners Credit and Fortress Investment Group were said to be considering a $1 billion investment. A group of wealthy individuals led by film producer Steven Paul, who were trying to put together a deal of their own, joined Bronfman. They accounted for several billion dollars more. But Bronfman’s backers started to drop out at the prospect of a bidding war with one of the world’s richest men, and he needed to deliver signed commitments ahead of an Aug. 28 deadline. One investor, who declined to be identified because the deal talks were private, said he left the group just days before the deadline. He couldn’t get comfortable with the $400 million breakup fee for Ellison, as well as the $16-a-share they were offering for a chuck of the company’s nonvoting stock. In the end, Bronfman gave up. At the same time Warburg Pincus and Blue Owl Capital were putting together financing for Byron Allen’s bid to acquire all of Paramount, according to people familiar with their discussions. They determined the troubles in Paramount’s cable-TV business were too great, particularly after the company took a nearly $6 billion writedown on those businesses earlier in August. Over the year or so that Paramount’s controlling stockholder, Shari Redstone, weighed selling the company, some of the biggest names around looked at Paramount, including Warner Bros., Sony Group, Apollo Global Management and Barry Diller. But, in the end, no major private equity firms or rival industry player made a serious bid. Did the king of cable stay in too long?John Malone is widely considered the king of cable TV. And it’s made him fabulously wealthy, with a net worth estimated by Bloomberg at $9.3 billion. But his positions in cable-related businesses have cost him in recent years as customers have canceled pay-TV subscriptions in favor of streaming services. He’s lost at least a couple billion dollars as these stocks retreated from their all-time highs. Liberty Broadband, which controls the nation’s No. 1 cable provider Charter Communications Inc., is trading two-thirds off its 2021 peak. Liberty Global, a top pay-TV provider in Europe, is down about 60%. Malone’s interests in the cable-TV programming side are doing even worse. Qurate Retail Inc., owner of QVC and the Home Shopping Network, is trading around 60 cents. The decline at Warner Bros. is 72%. Malone helped create the company two years ago with the merger of AT&T’s WarnerMedia business with Discovery, where he was a major investor. Malone is a board member at Warner Bros. and holds about 19 million shares of the company, the parent of TNT, CNN and other channels. Malone built Tele-Communications into the largest and most-feared player in the business before selling to AT&T Inc. in 1999 for $54 billion. Since then the 83-year-old as been wheeling and dealing as chairman of Liberty Media, a consortium of telecom and entertainment investments. Malone has diversified his portfolio, investing in the Atlanta Braves baseball team, Formula One car racing and the Sirius satellite radio network. He could still be ahead based on whatever his initial investments cost him. His current thoughts on cable-TV’s future aren’t immediately discernible. Malone turned down a request for an interview. Earlier this year, he accepted an award from the Singleton Foundation for Financial Literacy and Entrepreneurship. Liberty Global, he said, was buying back about 18% of its shares this year from internally generated funds. Warner Bros., which he said will “turn out to be very, very cheap,” is focused on reducing debt. “The time will come for the bigger fish to eat the smaller fish and generate synergies thereby,” Malone said. More bad music dataGrowth of the US music industry has slowed to a crawl this year. Domestic sales are on pace for their smallest gain since 2015. However, a major media analyst said now is the time to buy shares in Universal Music Group. The No. 1 tour in the world is…Tomorrow X Together. The Korean pop group grossed an average of $9.5 million a night from eight shows over the last few months. The average ticket price was, brace yourself, $387.74. Deals, deals, deals - ESPN extended its deal for the US Open tennis tournament. It will now carry the event through 2037.

- NFL owners voted to let private equity firms invest in their franchises.

- Paramount may sell up to a dozen TV stations while Amazon is exploring a sale of the division that produces The Voice and Shark Tanks.

- Disney is getting closer to merging its assets in India with Mukesh Ambani’s Reliance Industries. (Another major media merger in India officially died.)

- Private equity is setting its sights on the youth sports industry.

|