| The legal problem with President Donald Trump’s tariffs is that the United States has a Constitution, and the Constitution says that Congress has the power to impose tariffs and the president doesn’t. This is not some weird technicality; this is just what the Constitution says. “The Congress shall have Power To lay and collect Taxes, Duties, Imposts and Excises,” and “To regulate Commerce with foreign Nations.” But Congress did not pass President Trump’s “Liberation Day” tariffs on April 2, or any of the various up-and-down permutations since then. That was all him, acting by executive order. Congress did pass a law, in 1977, that gives the president powers to “deal with any unusual and extraordinary threat, which has its source in whole or substantial part outside the United States, to the national security, foreign policy, or economy of the United States, if the President declares a national emergency with respect to such threat.” (This law is called the International Emergency Economic Powers Act of 1977, or IEEPA.) Specifically, the president can “investigate, block during the pendency of an investigation, regulate, direct and compel, nullify, void, prevent or prohibit, any acquisition, holding, withholding, use, transfer, withdrawal, transportation, importation or exportation of, or dealing in, or exercising any right, power, or privilege with respect to, or transactions involving, any property in which any foreign country or a national thereof has any interest by any person, or with respect to any property, subject to the jurisdiction of the United States.” That long list is usually abbreviated, in this context, to “regulate … importation”: The IEEPA allows the president to regulate imports in an emergency. If he can regulate imports, can he impose tariffs on them? Eh, maybe, sounds like a regulation. And that is the legal theory behind Trump’s Liberation Day tariffs: - There is an “unusual and extraordinary threat” (trade deficits), so the president can declare that all US trade with every country is a national emergency.

- In an emergency, he has the power to regulate imports.

- He will regulate imports by imposing tariffs on them.

The specific words of the Constitution do not matter, because foreign trade is an emergency and the president must regulate it. We discussed this theory the day after Liberation Day, and again the following week. I don’t love it! As I wrote in April: The idea seems to be that every trade policy of every country in the world, over the past several decades, constitutes an “unusual and extraordinary threat.” This is a strange way to use words! How can every instance of trade with every country be unusual? How, after decades of trade deficits, is a trade deficit extraordinary? It is also a strange way to use law. The US is in a perpetual state of emergency with respect to every country forever, allowing the president to use emergency powers to bypass the Constitution to impose tariffs. We also discussed a doctrine of constitutional law called the “nondelegation doctrine,” which says that Congress cannot give up its constitutional legislative power to the executive. It can delegate some decisions to the executive, but only with an “intelligible principle” to guide the executive’s action. The executive can fill in the details of congressional legislation, but Congress can’t just tell the president “make any laws you want,” because the Constitution says that that’s Congress’s job. And so, I wrote, there are two possibilities here: - The IEEPA doesn’t actually give the president the power to impose tariffs on every country just because he doesn’t like free trade. IEEPA powers are only for emergencies, and “international trade exists” can’t really be an unusual and extraordinary threat to the US.

- If the IEEPA did give the president sweeping powers to impose tariffs, that would be unconstitutional.

This all struck me as obviously correct in principle, but I have become cynical about the Constitution actually controlling anyone’s actions here in 2025, so I called it “frankly pretty speculative” as a theory of actually stopping the tariffs. Still, worth a shot. And here you go! The bulk of President Donald Trump’s global tariffs were deemed illegal and blocked by the US trade court, dealing a major blow to a pillar of the Republican’s economic agenda. A panel of three judges at the US Court of International Trade in Manhattan issued a ruling Wednesday siding with Democratic-led states and a group of small businesses that argued Trump had wrongfully invoked an emergency law to justify some of his levies. The Trump administration filed a notice that it was appealing the ruling. The US Supreme Court may ultimately have the final say in the high-stakes case that could impact trillions of dollars in global trade. … The order suspends the vast majority of Trump’s tariffs — his global flat tariff, elevated rates on China and others, and his fentanyl-related tariffs on China, Canada and Mexico are all suspended by the ruling. Other tariffs imposed under different powers, like so-called Section 232 and Section 301 levies, are unaffected, and include the tariffs on steel, aluminum and automobiles. Here is the court’s opinion, which starts by laying out the issue pretty clearly: The Constitution assigns Congress the exclusive powers to “lay and collect Taxes, Duties, Imposts and Excises,” and to “regulate Commerce with foreign Nations.” U.S. Const. art. I, § 8, cls. 1, 3. The question in the two cases before the court is whether the International Emergency Economic Powers Act of 1977 (“IEEPA”) delegates these powers to the President in the form of authority to impose unlimited tariffs on goods from nearly every country in the world. The court does not read IEEPA to confer such unbounded authority and sets aside the challenged tariffs imposed thereunder.

Later the court uses the basic two-possibilities framework I laid out in April: Either IEEPA has no limits (and is therefore unconstitutional), or it has limits (so Trump can’t just impose whatever tariffs he wants on everyone): Underlying the issues in this case is the notion that “the powers properly belonging to one of the departments ought not to be directly and completely administered by either of the other departments.” Federalist No. 48 (James Madison). Because of the Constitution’s express allocation of the tariff power to Congress, see U.S. Const. art. I, § 8, cl. 1, we do not read IEEPA to delegate an unbounded tariff authority to the President. We instead read IEEPA’s provisions to impose meaningful limits on any such authority it confers. Two are relevant here. First, § 1702’s delegation of a power to “regulate . . . importation,” read in light of its legislative history and Congress’s enactment of more narrow, non-emergency legislation, at the very least does not authorize the President to impose unbounded tariffs. The Worldwide and Retaliatory Tariffs lack any identifiable limits and thus fall outside the scope of § 1702. Second, IEEPA’s limited authorities may be exercised only to “deal with an unusual and extraordinary threat with respect to which a national emergency has been declared . . . and may not be exercised for any other purpose.” 50 U.S.C. § 1701(b) (emphasis added). As the Trafficking Tariffs do not meet that condition, they fall outside the scope of § 1701.

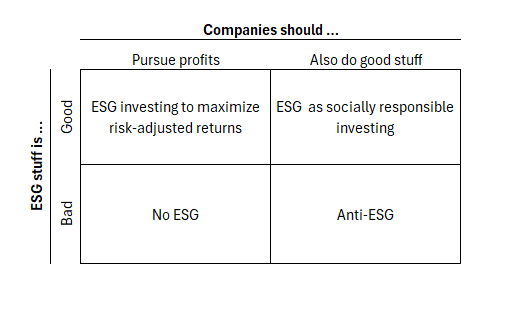

The court decides that “any interpretation of IEEPA that delegates unlimited tariff authority is unconstitutional”: To be a constitutional delegation of power, IEEPA has to impose some limits on the president’s powers to regulate trade. And “the President’s assertion of tariff-making authority in the instant case, unbounded as it is by any limitation in duration or scope, exceeds any tariff authority delegated to the President under IEEPA.” Again, this all seems pretty obvious to me but, uh, what happens next? The government will appeal; I find this opinion convincing, but there is an audience for the argument that the president can do whatever he wants. (“The Supreme Court may again prefer Trump to precedent,” writes UBS’s Paul Donovan.) There are statutes other than IEEPA that allow the president to impose tariffs in more limited circumstances and with more procedures and findings; presumably the government will try those. “Nothing’s really changed,” said trade adviser Peter Navarro. But those statutes are a bit narrower. “Republicans in Congress have advanced legislation that would give the president wide authority to impose so-called reciprocal tariffs,” reports Bloomberg, “but concern about the impact of Trump’s widespread levies is expected to limit the appetite for moving that measure now.” For now, though, will the tariffs just … go away? Just because they’re illegal? Is that how this works?  | | | I think there are four ways to think about environmental, social and governance (ESG) investing, and I have made you a chart: That is: You might have one of two views about the purpose of a corporation (or the purpose of investing). One view is that companies should maximize profits within the law and not pursue any social or moral ends; the other is that companies should also pursue some other pro-social goals. There is a roughly consistent set of goals (reducing carbon emissions, diversity, some other stuff) that are generally associated with the term “ESG.” Generally ESG investors would say that these are pro-social goals, but you could disagree. You might have a view that the environment should be several degrees warmer, and you might want companies to emit more carbon to warm things up. That would be a kind of environmental goal, but it would not be “ESG” in the conventional usage of the term. Or you might think that the risk of climate change is overstated and that reducing carbon emissions would be bad for human flourishing. Or you might think that companies overemphasize diversity and should stop. That would be a social position of yours, but it would not conventionally be an ESG position. You could use words in a different way — you could say “I am an ESG investor, meaning that I care about making the environment warmer and boards of directors less diverse” — but it would be unusual. And so there’s my matrix: - If you think that the standard ESG goals are good, and that companies should just pursue profits, that’s no problem! You can just invest normally and keep your ESG goals to yourself. But probably you will do something different: Your investments will be skewed toward companies with good ESG scores (companies that limit carbon emissions, have diverse boards, etc.), and you will push those companies to do more, because you will also have some tendency to think that the ESG goals are good for long-term shareholder value. “The climate is changing, so the world will transition away from fossil fuels, so I should invest in companies that will benefit from that transition; investing in coal companies is too risky.” [1]

- If you think that the ESG goals are good, and that companies have a duty to society beyond the pursuit of profits, you will invest in companies with good ESG scores and push them to pursue ESG goals for their own sake. Even if you think that pursuing ESG goals will reduce long-term shareholder value, you will want companies to pursue them (at least at some margin), because you are not just a shareholder: You are a human, you have to live on this planet, you want the planet to be nice, and companies have a role in making it nice that goes beyond the pursuit of profits.

- If you think that the ESG goals are bad, and that companies should just pursue profits, that’s also no problem. You can just invest normally and vote against ESG proposals, because you think they are bad and also not likely to increase profits. [2]

- If you think that the ESG goals are bad, and that companies have a duty to society beyond the pursuit of profits, you will do exactly what ESG investors do but in reverse. You will invest in companies and push them to drill more oil, etc., even if you think that will reduce long-term shareholder value, because you are a human, you live on this planet, you want the planet to be nice, and more oil would be nice.

People are very confused about these things, in part because it is often in their interests to be confused. And so, in the golden age of ESG investing, big asset managers were both saying that their ESG investing enhanced risk-adjusted returns, and implying that it was designed to make the planet better. There was some tension in those theories, but you can kind of blend them together for marketing purposes. And now, in whatever the opposite of a golden age of ESG investing is, people get confused the other way. Sometimes people argue that ESG investing necessarily violates fiduciary duties to asset holders, because ESG has to lower returns, which is really only true of one of the two ESG theories. More confusingly, though, people will argue both that companies should only pursue profits without regard to social goals, and that they should drill more oil in order to provide employment for Louisiana oil drillers or whatever. Those theories are inconsistent! Anyway here’s France: France issued one of Europe’s starkest calls yet for the financial industry to support defense companies, as the region shores up its security in face of Russian aggression in Ukraine. Banks should change their internal rules “so as to no longer systematically exclude defense, but also to voluntarily direct part of the savings entrusted to them toward this sector,” an economy ministry spokesperson said in response to questions from Bloomberg. European states are leaning on banks and investors to funnel money to arms manufacturers so that they can increase production. That’s sparking a reset at many financial firms, after years in which they shunned such companies and instead focused on supporting clients that fitted a narrower definition of being environmentally and socially sustainable. Traditional ESG principles would disfavor making bombs. France wants more bombs. Saying “stop doing ESG investing for bombs” might lead to more bombs: If you care only about the pursuit of profits, you will make profitable bombs, even if you think bombs are bad for society. But France is saying something more: Not just “no longer systematically exclude defense,” but also “voluntarily direct” money to defense. “Bombs are good for society, so make more of them, even if that does not maximize risk-adjusted returns.” There are more important things than profits. Yesterday I wrote about Congress’s proposed 21% excise tax on certain university endowment income, and I suggested my own homemade workaround, which is basically that big universities should put their operating expenses into for-profit subsidiaries so that they can be deducted against the endowment income. The idea would be that Harvard University would seed a for-profit company, the Chemistry Corporation, which would pay its chemistry professors and teach the classes and invest Harvard’s seed money to earn a return. That way, at least, the salaries of the chemistry professors would be deductible against the investment income, which would not be the case otherwise. Alas, a reader pointed out that the people who wrote the excise tax thought of that. Section 4968(d) of the Internal Revenue Code says that “assets and net investment income of any related organization with respect to an educational institution shall be treated as assets and net investment income, respectively, of the educational institution,” and a “related organization” includes any organization controlled by the institution. So if Harvard parked some endowment assets in a for-profit corporation, its investment income would still be attributed to Harvard, and it would still have to pay the excise tax. [3] But readers emailed me three other proposals, which are arguably simpler. None of them are tax advice! But here you go. First: The excise tax applies only to schools with “at least 500 tuition-paying students” and an endowment of at least $500,000 per student. The biggest targets have thousands of tuition-paying students. But, you know. Nick Parillo emailed [4] : With a current 1.4% endowment tax, all schools are much better off eating the tax and continuing to charge tuition to more than 500 students, but with a proposed 21% rate, some of the targeted schools would be much better off simply abolishing tuition — still collecting fees for room and board? increasing fees for room and board? — and avoiding the tax. Back of the envelope example: In 2024, Princeton collected [$137 million] in net tuition and fees, compared to [$1,715 million] in endowment distributions (which would generate a tax liability of roughly [$360 million]).

“Their endowments are so big that they could stop charging tuition” is a long-time criticism of the big rich universities, but in a 21% tax regime it would actually save them money. Second: The excise tax applies to educational institutions, not other charities. Not, for instance, donor-advised funds or charitable trusts. So if you give money to Harvard, you will get a tax deduction, Harvard will pop the money into its endowment, and any earnings on that money will be taxable. But if you give that money to your own donor-advised fund, you will get a tax deduction today, you can invest the money, and any earnings will be non-taxable. And then over time you can distribute it to Harvard for its operating expenses, which will also be non-taxable. (Also you can pick where to invest it, which might be appealing if you don’t like Harvard’s investing policies.) And so Kelly Shue emailed: If Harvard remains a non-profit subject to endowment taxes, donors could instead establish a donor-advised fund, let the fund’s investments grow tax-free, and then make grants to Harvard for immediate use — thereby avoiding any taxable endowment income.

This doesn’t fix the problem of existing endowments, which are pretty big, but I can say from personal experience that Harvard and Yale continue to fundraise, so I guess growing the endowments is still a goal. Arguably it shouldn’t be. Arguably “get each alumni class to set up a charitable fund that takes donations, invests them, grows tax-free and makes annual donations to the operating budget” should be. [5] The third reader idea is the simplest: Just become a for-profit company. Under the tax proposal, a rich nonprofit university pays higher taxes than a for-profit company (because it pays taxes on all investment income, without being able to deduct operating expenses), so the big universities could become for-profit companies and pay lower taxes. This would cut off their main source of fundraising (tax-deductible donations), but would open up a huge new source of fundraising: selling stock. Obviously there is a problem with repurposing the existing huge endowments for for-profit purposes but, you know, if OpenAI can figure it out probably Harvard can. Public credit is the new private credit | One much-cited advantage of private credit is that, if you borrow from private credit funds, you have a relationship with your lenders. You negotiate a loan with a limited number of private credit funds, and they plan to hold the loan to maturity. It doesn’t trade, so it won’t end up in the hand of activists or vulture-y distressed debt funds. If you run into financial trouble, you will go back to the nice people who loaned you the money in the first place, and they will sympathize and try to work with you rather than saying “tough luck, we own your company now.” Whereas if you borrow in the bond or broadly-syndicated-loan markets, your debt trades freely, and you might wake up one day and find that it is owned by some pretty tough customers. I have always assumed that this is a continuum, and that in the long run private credit will trade a bit more, while syndicated loans will maybe trade a bit less. If you really don’t want someone to own your debt, the market will provide a solution. Here’s a Bloomberg News story about disqualified lender lists: Clearlake Capital Group … has expanded the so-called disqualified lender list for [its portfolio company] container manufacturer Pretium Packaging to almost 100 names in recent weeks, according to people with knowledge of the matter. Typically such lists, which allow borrowers to block certain parties from purchasing their loans, range from a handful of shops to a few dozen, market watchers say. Blacklists have become a common strategy for company owners that are weighing a potential restructuring to avoid dealing with money managers they consider difficult to negotiate with, and are often used to counter the most aggressive “loan-to-own” players. But Clearlake is pushing the tactic to the limit after an investor that had made it known it was seeking to take over Pretium got close to acquiring a significant chunk of the company’s debt via a block trade, according to one of the people familiar with the situation. In response, Clearlake vastly expanded its ban list, in part to prevent a similar situation from occurring in the future, and the trade ultimately never went through, the person added. Bloomberg couldn’t confirm the prospective investor. A Loomis Sayles & Co. portfolio manager says: “It seems like an intentional strategy to make something that has historically been public almost private,” and, yes, of course. Private credit is hot right now; obviously public credit will copy it. Classically the way insider trading works is that there is an insider and an outsider. The insider works at a public company and has material nonpublic information about a merger or earnings or whatever, but if he traded on that information everyone would notice and he would get in trouble. The outsider is a brother-in-law or college roommate or golf buddy of the insider; the insider gives the inside information to the outsider, who trades on it, with some plausible deniability. The outsider makes a lot of money buying short-dated out-of-the-money call options on a merger target. But what does the insider get? The insider had the valuable information and took risks to give it to the outsider, but the outsider is the one who made money. Shouldn’t the insider get a cut? One possible answer is “no, the insider is really fond of his brother-in-law, so he just wanted to see him happy and didn’t need any other reward.” Another is “the brother-in-law is kind of a moocher anyway, and by giving him this stock tip the insider avoided getting hit up for a loan at Christmas.” The most classic solution is that the outsider cashes out his profits in $100 bills, puts half of them in a paper bag, and hands the bag to the insider in a parking lot. More generally, the outsider often shows his gratitude to the insider by giving him something of monetary value. We once talked about an insider trading case where the outsider allegedly paid for the insider’s family “to travel from Saint Barthélemy to Nantucket using a private jet,” which feels right. Should the outsider go to a bank and get a cashier’s check for half of the profits and hand it to the insider? I mean. No? But nobody should do any of this so what do I know. Anyway here’s a criminal insider trading case against Rouzbeh “Ross” Haghighat, who was on the board of directors of Chinook Therapeutics Inc. when it was acquired by Novartis AG. Haghighat allegedly did a little trading himself (allegedly buying 40 shares of Chinook in his daughter’s account, for a profit of approximately $556.80), but mostly he is accused of tipping various friends and relatives. One of them is Kirstyn Pearl, his step-daughter, who allegedly spent $5,505 buying short-dated out-of-the-money call options on Chinook, and quickly made a profit of $114,081 when the deal was announced. Good trade! “I’m glad this worked out honey,” Haghighat texted her, and she replied “So glad it worked out as well — very very grateful.” But they kept texting about, as prosecutors say, “splitting the proceeds of PEARL’s illicit profits,” with Haghighat saying “Kirst, I’d like to close the loop on fund transfer this week. Easiest is to write out a check or transfer to me and I’ll redirect into individual accounts.” So she gave him a $55,015 cashier’s check, “which ROSS HAGHIGHAT later claimed in messages to PEARL that he lost.” She had to get a new check, it was a whole thing. Eventually he got his money though. And then: On or about April 24, 2024, PEARL messaged a family member concerning the purportedly missing check, and said, in part: “I just totally had a brain popping realization — you know how SOMEHOW a $60k check went missing … it was intentional — since it was an illegal insider trading move.” … Later in the message thread, PEARL told the family member, “Delete this lol.”

I don’t think this makes any sense — he deposited the replacement check! — but, sure, if you are splitting the proceeds of illegal insider trading I guess it might be wise not to get a bank check. Not legal advice! Also don’t text about it! The ‘TACO Trade’ That Has Trump Fuming. Musk Exits DOGE Leaving Threadbare Agencies and Strained Workers. Japan Bonds Draw Weak Demand as Rise in Superlong Yields Sparks Concern. Exxon to Operate Guyana ‘Business as Usual’ If It Loses Chevron-Hess Arbitration. Elon Musk Tried to Block Sam Altman’s Big AI Deal in the Middle East. 1MDB scandal exposer seeks $18mn from ex-Goldman executive. VC Funds Are for Sale — at a Discount. UniCredit to Double Stake in Greece’s Alpha Bank to Around 20%. ECB governing council member convicted of bribery. “The goal is to break [Harvard], then break peer institutions, and ultimately break American civil society — to create a situation where the idea that an institution has legal rights is irrelevant, because to defy Trump is to invite ruin even if you can eventually win in court.” Lawyer Murdered Client in 2013 to Delay Start of Her Divorce Trial, Prosecutors Say. If you'd like to get Money Stuff in handy email form, right in your inbox, please subscribe at this link. Or you can subscribe to Money Stuff and other great Bloomberg newsletters here. Thanks! |